Investments into clean energy has increased because of following reasons:

1. Russia’s invasion of Ukraine and urgency felt by westerns to build resilience in their energy supply sources

2. Inflation reduction act of US

3. Fear of not being able to meet 1.5 degree C

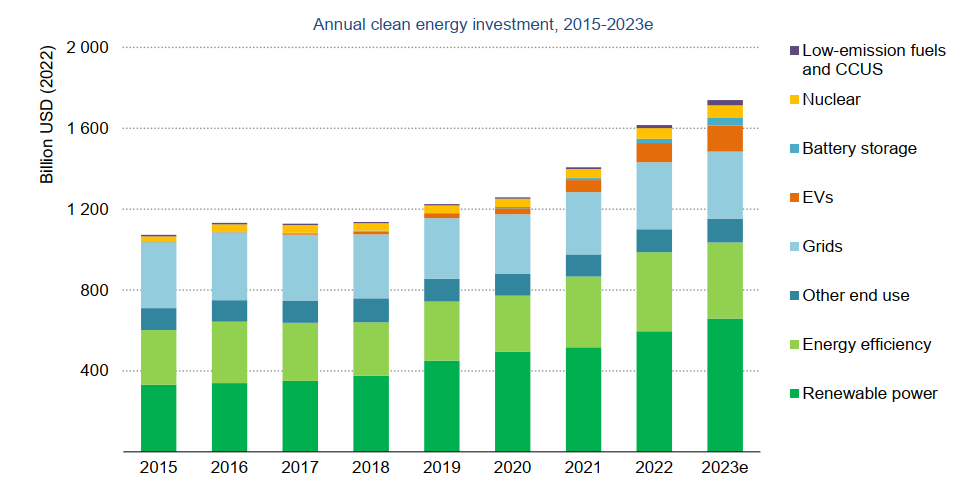

For past 7 years (2015-2022), cumulative investment into clean energy sources triumphs those into fossil fuels by close to 20%. The ratio has been increasing over the past 7 years and is expected to follow the trend in coming years.

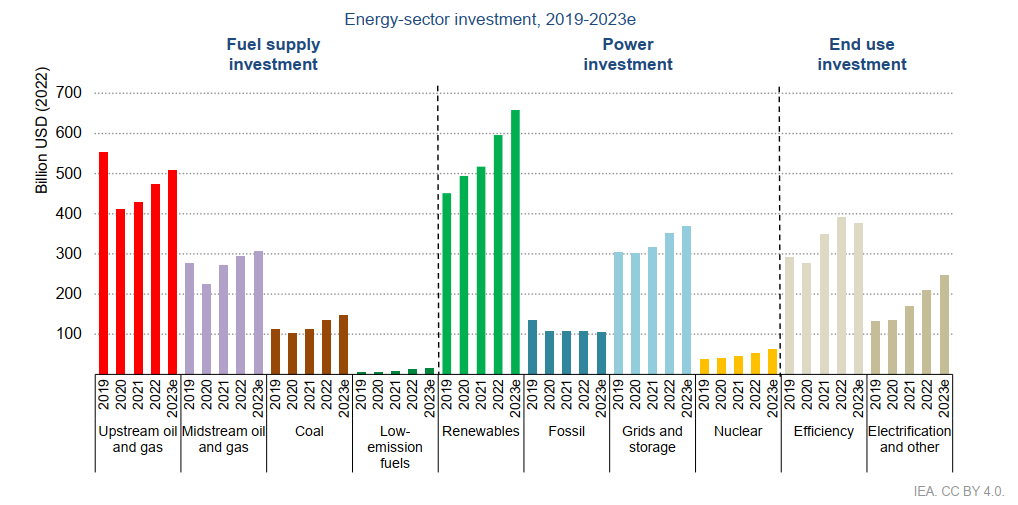

Energy sector Investments can be typically characterized into three buckets:

1. Fuel supply investment- Upstream Oil and Gas, Midstream Oil and Gas, Coal, Low-emission fuels

2. Power Investment- Power, Fossil, Grids and storage, Nuclear

3. End Use Investment- Efficiency, Electrification and other

Renewables led by solar, and EVs are leading the expected increase in clean energy investment in 2023.

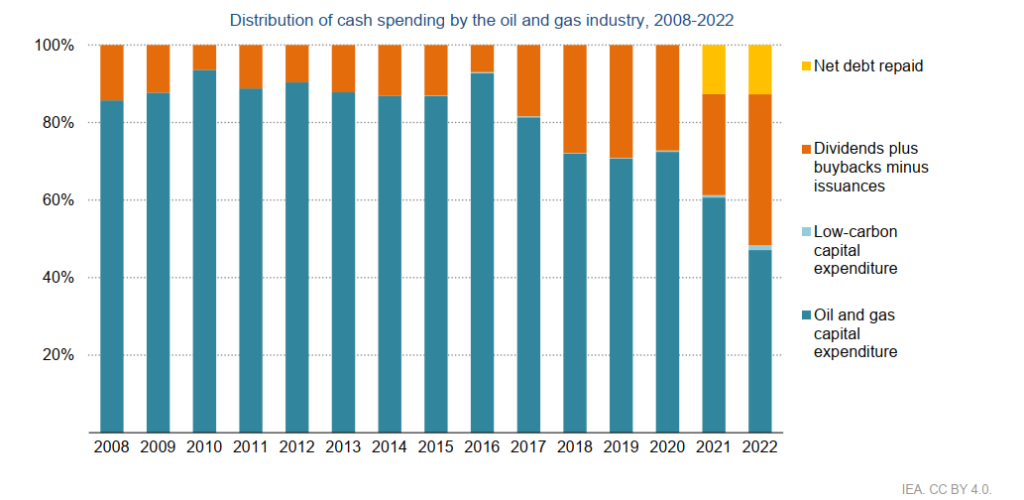

Reinvestments, another important gauge of forecasting growth points to a dissappointing picture for oil and gas industry. Reinvestment by Oil and Gas companies into upstream and mid-stream avenues have come down to less than 50% for CY2022. This figure used to above 80%, a decade back. A lot of free cash flow is going into repaying debt, paying out dividends, exercising buybacks and some into low carbon capex.

Close to 2.8 tn USD will be invested in energy in 2023. 1.7 tn USD will go into clean energy sources (renewable power, nuclear, grids, storage, low- emission fuels, efficiency improvements, and end-use renewables and electrification). The remainder slightly over 1 USD trillion is going to unabated fossil fuel supply and power of which around 15% is to coal and the rest to oil and gas. Five years ago this ratio was 1.1.

Interestingly, Consumers are investing in more electrified end uses. Demand for electric cars is booming, with sales expected to leap by more than one-third this year after a record-breaking 2022. As a result, investment in EVs (defined as the incremental spending on EVs vs the average price of vehicles sold in a given country) has more than doubled since 2021, reaching USD 130 billion in 2023.

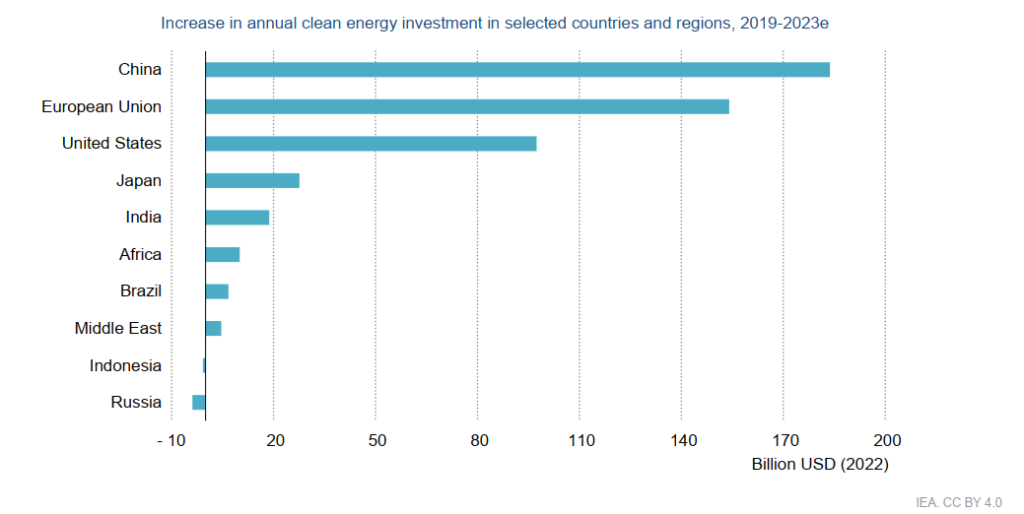

One area of concern is that new investments in clean energy spending in recent years, although impressive, has been concentrated in a handful of countries with China leading the pack followed by European Union, United States, Japan and India.

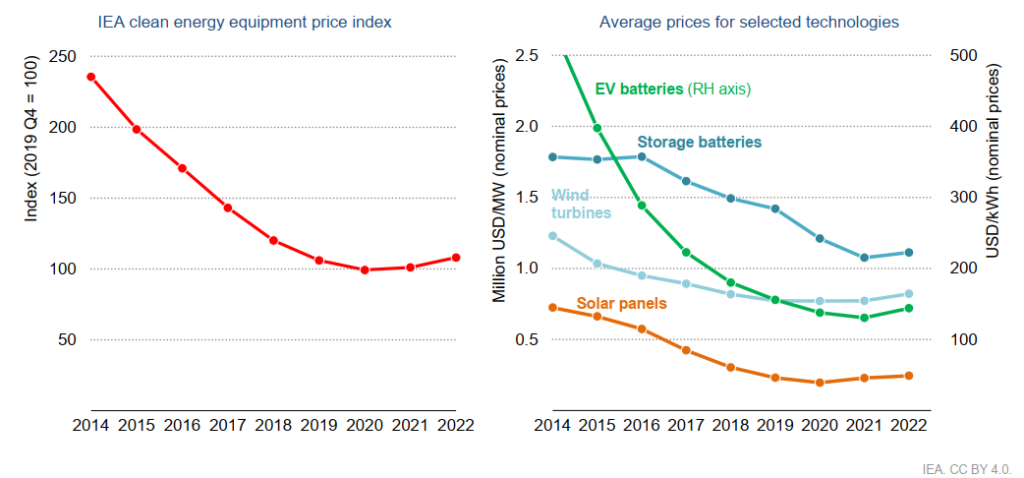

Cost side concerns- Clean energy costs edged higher in 2022 but pressures are easing in 2023 and mature clean technologies remain very cost competitive in today’s fuel price environment.

Competition for clean energy manufacturing and for supplies of critical minerals and metals is a major issue for the resilience of transitions:

Record sales of EVs, strong investment in battery storage for power (which are expected to approach USD 40 billion in 2023, almost double the 2022 level) and a push from policy makers to scale up domestic supply chains have sparked a wave of new lithium-ion battery manufacturing projects around the world. If all capacity announcements were to materialize, then 5.2 TWh of new capacity could be available by 2030. For the moment, China is the main player at every stage of global battery manufacturing, with the exception of the mining of critical minerals

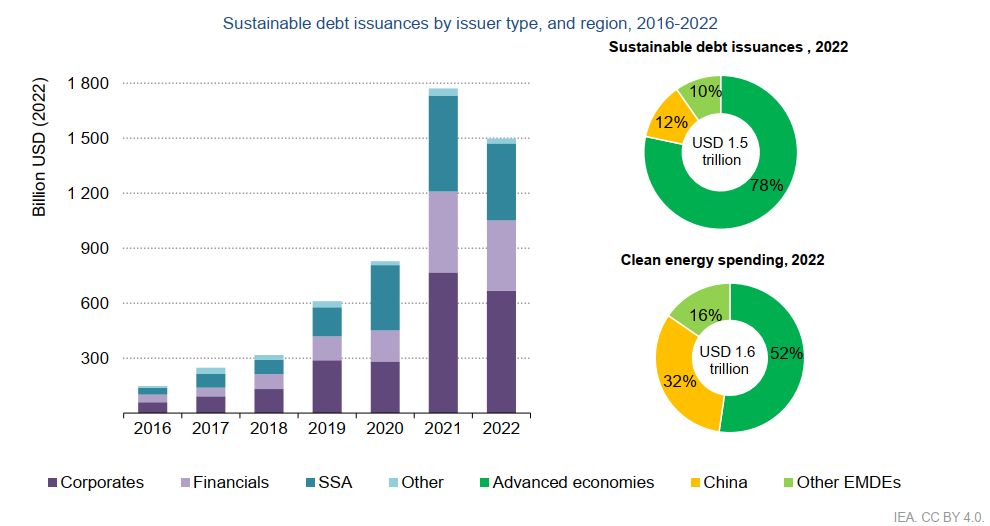

Sustainable Financing Scenario

Expanding access to finance will be vital: sustainable finance has weathered the storm of the

energy crisis, but remains heavily concentrated in advanced economies